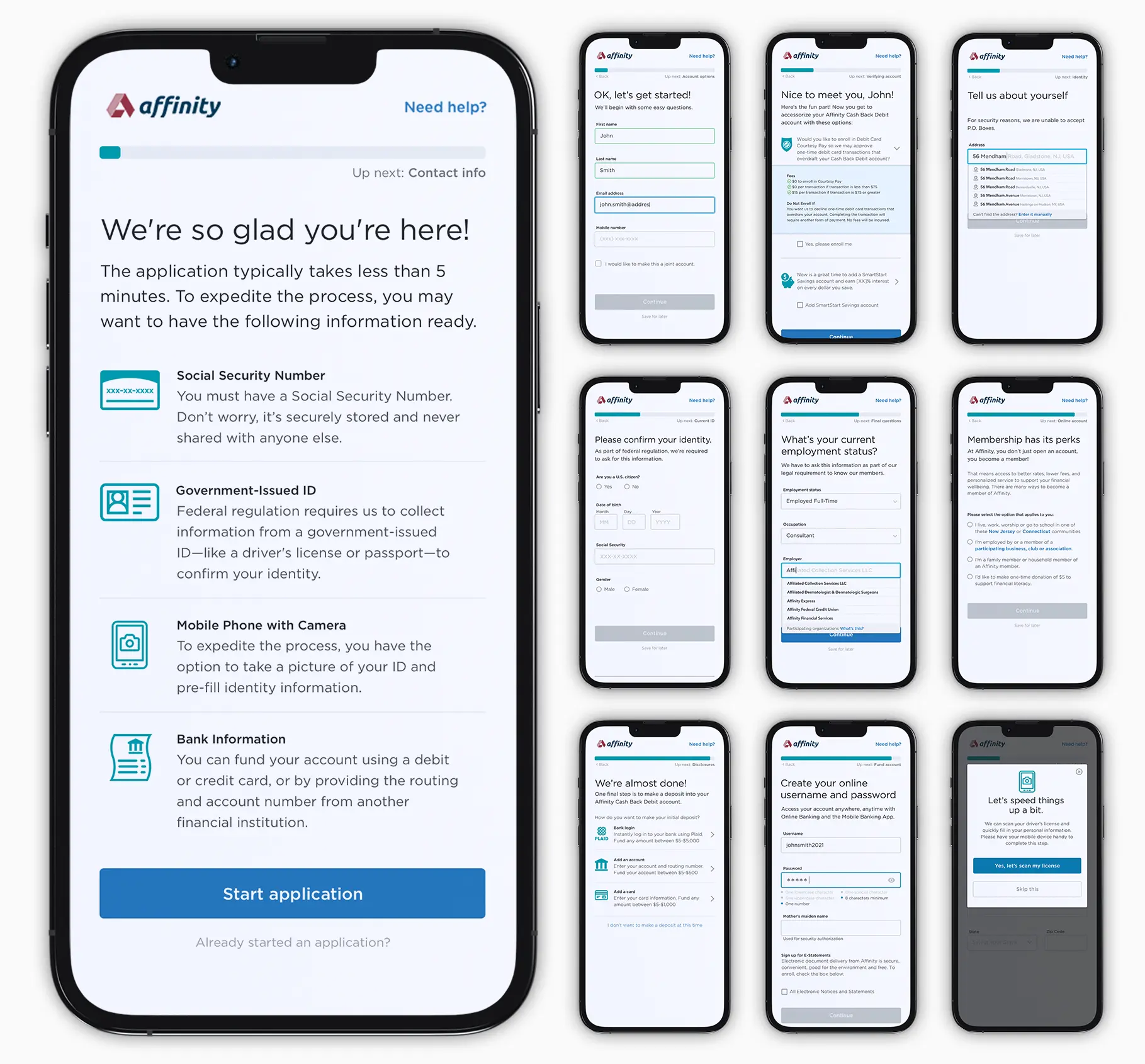

For many banks, digital account opening remains a difficult challenge despite all the investment in digital transformation. Even though digital onboarding remains a strategic objective for banks year after year—with 46% of financial institutions planning to enhance their existing digital account opening services in 2021—few are seeing tangible results.

Most legacy banks invested heavily in the technology that underpins new onboarding processes, but unlike the upstarts, have failed to rethink the processes themselves. That is why they are falling behind, and that is why customers are still failing to complete applications.